The United Arab Emirates is rapidly transitioning toward a fully digital tax environment where invoices are no longer treated as mere financial documents but as structured compliance records. The upcoming e-invoicing initiative, spearheaded by the UAE Federal Tax Authority (FTA), represents a fundamental shift in how commercial transactions are generated, validated, and reported.

This regulatory evolution mandates that every invoice follows specific structured data standards to ensure traceability and alignment with digital reporting requirements. Unlike earlier VAT implementations that focused on periodic summary reporting, this new framework introduces transaction-level visibility and system-led compliance. As a result, finance operations, ERP architectures, and audit readiness across all organisations will be directly impacted.

UAE Digital Transformation Is Reshaping Financial Compliance

Digital governance in the UAE has reached a pivotal stage where the focus has moved beyond basic record keeping to real-time financial transparency. While the initial VAT implementation established the foundation for tax reporting, the next phase aligns the UAE with global digital tax frameworks designed to reduce fraud, improve data accuracy, and enable automated compliance.

UAE’s Shift Toward Real-Time Financial Transparency

The traditional model of invoice generation, where documents were created in isolated accounting systems and later summarised for quarterly VAT filing, is being replaced.

The new regulatory model requires invoices to be generated in structured, machine-readable formats such as XML or specific JSON schemas. These formats allow immediate digital validation and the creation of immutable audit trails.

Key changes include:

- Transaction-level traceability where every sale or service is tracked at line-item level, giving the FTA granular visibility into business activity.

- Automated tax validation where systems check VAT rates, exemptions, and calculations at the point of entry.

- Invoice authenticity verification using digital signatures and unique identifiers to prevent tampering after issuance.

- Compliance at the point of creation requiring finance teams to ensure tax mapping and data accuracy from the start.

This transition requires operational transformation across the organisation. Standardised data frameworks must now govern all departments, from sales teams preparing quotes to procurement teams processing purchase orders. The entire lifecycle of a transaction must remain within regulated digital parameters.

Why Traditional Invoicing Processes Are Being Phased Out

Traditional invoicing workflows that rely on spreadsheets, manually created PDFs, and email-based approvals are no longer compatible with modern digital tax requirements.

While these methods were sufficient in the past, they lack the structured validation logic needed for automated compliance.

Data Structure vs Visual Formatting

E-invoicing frameworks prioritise structured data over document appearance. A PDF is only a visual representation of an invoice. The FTA requires the underlying structured tax data and digital identifiers.

Critical Limitations of Manual Workflows

Manual processes introduce risks such as VAT miscalculations, missing Tax Registration Numbers, and duplicate invoice numbering. These issues can trigger compliance flags during digital audits.

Traceability and Linking

Advanced compliance requires system-generated links between original invoices and related credit notes. Manual systems often fail to maintain consistent relationships between original documents and their corrections.

Operational Unsustainability

As the FTA moves toward Continuous Transaction Controls, manual reconciliation and adjustments will become increasingly impractical. High-volume, high-precision reporting cannot be maintained through manual intervention.

Businesses must therefore transition to system-generated invoices that integrate directly with regulatory frameworks, ensuring that every transaction is compliant by default.

UAE Tax Compliance Is Entering a New Digital Phase

The UAE tax framework is evolving from periodic self-assessment to continuous transaction monitoring. Compliance is no longer a monthly or quarterly activity but a continuous operational requirement.

From VAT Filing to Continuous Transaction Controls

Under the Continuous Transaction Controls model, the FTA gains near real-time visibility into business transactions. This significantly reduces post-filing corrections but increases the need for accuracy at the point of data entry.

Key requirements include:

- Automated tax logic where systems apply correct tax codes based on product type, supply location, and customer classification.

- Sequential invoice numbering enforced by systems to prevent gaps that could indicate unreported revenue.

- Automated audit trails that record every modification to financial data for regulatory review.

- High data consistency across customers, products, and multi-entity structures to ensure ERP and reporting alignment.

What This Means for UAE Businesses

Businesses must evaluate readiness across three core areas: process readiness, system readiness, and data readiness. The platform you rely on to manage these areas will determine how smooth or disruptive this transition becomes.

If invoices are still generated through disconnected tools or manual templates, the transition to structured compliance will cause significant operational disruption.

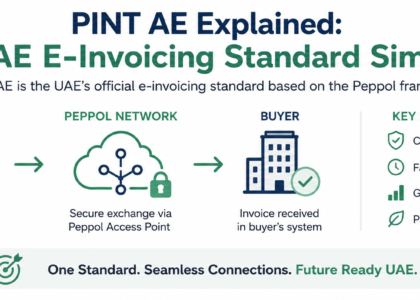

Understanding the UAE FTA E-Invoicing Initiative

The FTA e-invoicing initiative is designed to standardise invoice data exchange between taxpayers and the authority. The goal is to ensure consistent digital compliance and improve auditability across all businesses operating in the UAE.

What UAE E-Invoicing Means in Practice

In practice, e-invoicing requires invoices to originate from systems capable of generating structured data output.

This is especially important for businesses with:

- High-volume billing environments

- Recurring subscription models

- Intercompany and multi-branch transactions

- Complex multi-currency operations

For many organisations, this will require a shift from decentralised invoicing to centralised, system-led invoicing to maintain consistency across the enterprise.

UAE FTA E-Invoicing Implementation Timeline

The FTA has defined a phased rollout approach to allow businesses sufficient time for preparation.

| Milestone | Date |

| Voluntary pilot phase begins | 1st July 2026 |

| ASP appointment deadline, Phase 1 (AED 50M+ revenue) | 30th October 2026 |

| Mandatory go-live, Phase 1 | 1st January 2027 |

| ASP appointment deadline, Phase 2 (Below AED 50M revenue) | 31st March 2027 |

| Mandatory go-live, Phase 2 | 1st July 2027 |

| Government entities | 1st October 2027 |

UAE FTA E-Invoicing Registration Deadlines and Urgency

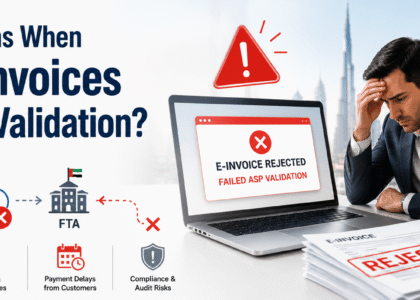

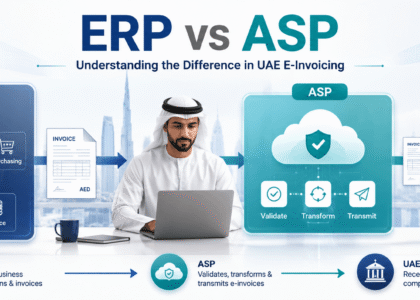

The Accredited Service Provider plays a central role in compliance. It acts as the technical bridge between enterprise systems and the FTA platform.

Its responsibilities include validating structured invoice data, ensuring correct formatting, and transmitting records to the FTA.

Large businesses that fail to appoint an ASP by 31 July 2026 risk missing the mandatory go live phase beginning 1 January 2027.

What This Means for UAE Businesses Moving Forward

The initiative marks the end of manual compliance. Businesses relying on spreadsheets or fragmented invoicing systems will face significant risks as their documents may no longer be recognised as valid tax records.

Why ERP Readiness Matters

The ERP system is now central to tax compliance. A compliant ERP must be capable of:

- Generating structured XML or JSON data aligned with FTA specifications

- Applying standardised VAT rules without manual intervention

- Scaling across high transaction volumes while maintaining data integrity

Without these capabilities, compliance becomes an administrative burden and increases the risk of penalties or rejected invoices.

The Need for System Led Compliance

A system led compliance model provides benefits that extend beyond regulatory requirements.

Organisations adopting this approach will benefit from:

- Improved financial visibility through real time data

- Faster internal approval cycles through automation

- Reduced reconciliation workload due to source level validation

- Stronger audit readiness through automated traceability

Preparing for the Next Phase of UAE E-Invoicing

Understanding the regulatory framework is only the first step. The next step is ensuring internal systems, especially ERP architecture and integration layers, are fully prepared.

Before the July 2026 pilot phase, businesses should:

- Review current invoice generation workflows

- Assess ERP capability for structured data output

- Identify manual dependencies such as spreadsheets and PDFs

- Validate tax data accuracy including TRNs and product codes

- Consult integration specialists for ASP connectivity requirements

Early preparation is essential to minimise compliance risk and ensure a smooth transition into the UAE digital tax environment.

While regulatory timelines provide clarity on when changes will take effect, the real challenge for businesses lies in understanding how these requirements translate into day-to-day operational and system changes.

At the core of this transformation is the readiness of enterprise systems to handle structured, real-time tax data without manual intervention. This is not limited to compliance teams alone. It impacts how invoices are generated, how data flows across departments, and how ERP systems interact with external validation frameworks.

To fully prepare for this shift, organisations must go beyond conceptual understanding and evaluate ERP readiness for e-invoicing across ERP environments, integration layers, and internal workflows.

This leads directly to the next critical stage of the transformation journey, where the focus moves from regulatory awareness to system level readiness and operational execution. For organisations looking for UAE FTA E-Invoicing Technical Implementation at this stage, the next phase explores how these requirements translate into architecture, workflow design, and system integration within ERP platforms.

Conclusion

The UAE’s move toward structured e-invoicing represents a fundamental shift in how businesses manage financial compliance. What was once a periodic reporting requirement is now evolving into a continuous, system driven process where accuracy, structure, and real time validation are essential.

For businesses operating in the UAE, this transition is not optional. It requires a clear understanding of how invoicing processes, tax logic, and enterprise systems must evolve to align with the Federal Tax Authority’s digital framework.

Organisations that begin preparing early will be better positioned to reduce operational disruption, maintain compliance confidence, and adapt smoothly to the upcoming regulatory phases.

The next stage of this transformation focuses on how these requirements are implemented within ERP systems and integrated across business functions to ensure seamless compliance at scale.

Frequently Asked Questions on UAE FTA E-Invoicing and Digital Tax Compliance

Is e-invoicing just sending a digital PDF?

No. A PDF is a visual document, a person reads it, but a computer can’t reliably extract structured data from it. E-invoicing requires machine-readable structured data, in XML format, that systems can validate and process automatically without a person opening the file. This is the core shift: invoices become data records first, documents second.

Is manual or spreadsheet-based invoicing still allowed?

No, not once you’re within your mandatory phase. Manual and spreadsheet-based invoicing can’t produce the structured, validated data the FTA requires. Businesses relying on these methods will need to move to an ERP or accounting system capable of structured data generation before their go-live date.

What should businesses do to prepare right now?

Start by reviewing how invoices currently move through your organisation and identifying every system or manual process involved. From there, evaluate your ERP readiness across three areas: process, system, and data.

For the full compliance timeline by business size and what happens if you miss it, see our e-invoicing ERP integration service page. For the specific systems and data checks your ERP needs, see our ERP Readiness guide.