Most UAE e-invoicing compliance failures are not caused by businesses ignoring the mandate. They are caused by businesses assuming they are ready when they are not. Here are the mistakes that consistently surface during implementation, and how to avoid them before they cost you.

With the ASP appointment deadline now set at 30 October 2026 and mandatory live invoicing following in January 2027, businesses across the UAE are moving from planning into active preparation. And that is where the problems tend to start.

The UAE e-invoicing framework is precise. Invoices are validated automatically against a defined set of rules before they are accepted into the exchange network. There is no human reviewer who will overlook a formatting inconsistency or an incomplete field. If the invoice does not pass validation, it does not move. That has real consequences for your billing cycle, your VAT records, and your trading relationships.

The mistakes below are not edge cases. They are the most common compliance errors that surface when businesses move from awareness to implementation, drawn from patterns seen across e-invoicing rollouts in other markets that have followed a similar Peppol-based framework.

The most common UAE e-invoicing mistakes

1. Assuming your ERP is ready without actually checking

The most frequent starting point for compliance problems is a business that assumes its ERP or accounting software will handle e-invoicing because it already handles invoicing. These are not the same thing. Generating a PDF invoice and generating a valid PINT AE structured XML invoice are fundamentally different outputs. Many ERP systems, even well-known ones, require configuration updates, version upgrades, or additional modules before they can produce compliant output.

What to do instead: Run a proper ERP readiness assessment before making any other decisions. It takes the guesswork out of your implementation timeline.

2. Missing or incorrect Tax Registration Numbers (TRN)

TRN validation is one of the first checks an Accredited Service Provider runs on every invoice. If the supplier TRN or buyer TRN is missing, formatted incorrectly, or does not match FTA records, the invoice fails immediately. Many businesses discover during testing that their customer master data has TRN gaps, particularly for older accounts that were set up before VAT registration became standard practice.

What to do instead: Audit your customer and supplier records specifically for TRN completeness and accuracy before you begin integration testing. This is a data quality task, not a technical one, and it takes longer than most businesses expect.

3. Incorrect VAT calculations at line-item level

PINT AE requires VAT to be calculated and reported at the individual line-item level, not just as a total at the bottom of the invoice. Some ERP configurations calculate VAT as a lump sum across the whole invoice. Others apply rounding in ways that create discrepancies between line-level totals and invoice totals. Both will fail validation rules.

What to do instead: Review how your ERP calculates and reports VAT at line-item level specifically. If it only reports a total, that configuration will need to change before invoices can pass ASP validation.

4. Waiting for your ERP vendor to handle everything

A common compliance delay comes from businesses waiting for their ERP vendor to release a UAE e-invoicing update and treating that as the end of the task. The vendor update, when it arrives, typically provides the technical capability to generate PINT AE output. It does not configure that output for your specific data, map your invoice fields to the correct XML elements, connect your system to an ASP, or test the end-to-end flow. That work still needs to happen on your side.

What to do instead: Track your vendor’s update timeline, but do not let it define your compliance timeline. Begin data preparation and ASP selection in parallel.

5. Leaving ASP appointment to the last month

The 30 October 2026 date is the deadline to appoint an Accredited Service Provider, not to complete your integration. ASP onboarding involves registration, technical setup, and end-to-end testing. Businesses that start this process in September or October will almost certainly run out of time to complete testing before the appointment deadline, and will then face a gap between their legal appointment and their actual operational readiness for January 2027.

What to do instead: Begin ASP evaluation and selection at least three to four months before the appointment deadline. Onboarding takes time even when everything goes smoothly.

6. Duplicate invoice numbers

PINT AE requires every invoice to carry a unique invoice number. If your ERP has ever reset its invoice numbering sequence, for example at the start of a financial year or after a system migration, there may be duplicate numbers in your historical records. The validation system will reject any invoice with a number that has already been used within your business’s invoicing records on the network.

What to do instead: Review your invoice numbering logic before going live. Establish a clear, non-resetting sequence for all e-invoices issued under the mandate.

7. Treating credit notes and debit notes as separate from the mandate

Some businesses focus their e-invoicing preparation entirely on outgoing sales invoices and overlook credit notes and debit notes. Under the UAE mandate, these document types are also subject to PINT AE formatting and ASP transmission requirements. A credit note issued as a PDF against a compliant e-invoice will create a compliance gap in your VAT records.

What to do instead: Map all invoice document types in your ERP, including invoices, credit notes, and debit notes, to PINT AE requirements during your readiness assessment rather than as an afterthought.

8. Skipping end-to-end testing before go-live

Configuring your ERP to generate PINT AE output and connecting it to an ASP are necessary steps, but neither confirms that your actual invoices will pass validation in a live environment. Differences between test data and production data, edge cases in your invoice types, and rounding inconsistencies only surface during end-to-end testing with real invoice samples. Skipping this step and going live directly is one of the most avoidable causes of post-go-live invoice rejections.

What to do instead: Build end-to-end testing into your implementation plan with a representative sample of your actual invoice types, including any unusual line-item configurations or tax categories your business uses.

A pattern that appears repeatedly across e-invoicing rollouts in other markets: businesses that tested thoroughly before go-live had significantly smoother transitions than those that treated testing as optional. The validation rules do not make exceptions for businesses that ran out of time to test properly.

What happens if invoices fail validation after the mandate is live?

Once mandatory e-invoicing takes effect for your business, invoices that fail ASP validation or that are issued outside the exchange network will not have legal standing as tax records under UAE law. That means your customers cannot use them to reclaim input VAT. It means your own VAT reporting will have gaps. And it means your trading partners, particularly larger enterprises, may be unable to process or pay those invoices.

The consequences compound quickly in high-volume billing environments. A configuration error that causes a portion of your invoices to fail validation is not a minor inconvenience. It is a significant operational and compliance problem that requires emergency remediation while your billing cycle continues to run.

Non-compliant invoices after the FTA mandate goes live carry the risk of financial penalties, VAT reporting discrepancies, and rejection by trading partners. The FTA has the authority to audit tax records and issue penalties for non-compliant invoice practices. Always verify the latest penalty framework directly at tax.gov.ae.

A pre-implementation checklist to reduce compliance risk

Before you go live — key checks

| ✓ ERP readiness assessment completed — PINT AE XML output confirmed or gap identified |

| ✓ Customer and supplier TRN data audited and cleaned across all active accounts |

| ✓ VAT line-item calculation logic reviewed and confirmed correct |

| ✓ Invoice numbering sequence reviewed with no duplicates or resets |

| ✓ All invoice types mapped — invoices, credit notes, debit notes |

| ✓ ASP selected and onboarding started well ahead of the October 2026 deadline |

| ✓ End-to-end testing completed with a representative sample of real invoice types |

| ✓ Validation failure process understood — team knows what to do when an invoice is rejected |

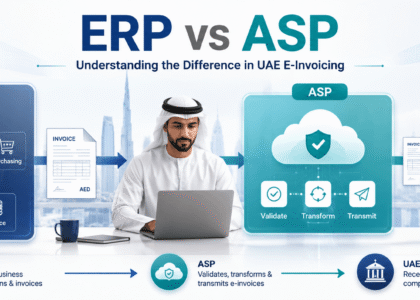

If you are unsure which of these gaps apply to your current setup, understanding where your ERP ends and your ASP begins is the right place to start before working through the list above.

Frequently Asked Questions

Why are UAE e-invoices rejected?

The most common rejection causes are missing or incorrect TRN data, VAT calculations that do not match line-item totals, incorrectly formatted XML output, duplicate invoice numbers, and mandatory fields that are absent or empty. All of these are caught at the ASP validation stage before the invoice enters the exchange network.

What are the most common UAE e-invoicing compliance mistakes?

Assuming ERP readiness without testing, poor customer TRN data, late ASP appointment, skipping end-to-end testing, and not mapping credit notes and debit notes to the mandate requirements. All of these are avoidable with a structured implementation plan that starts early enough.

What causes invoice validation failures in UAE e-invoicing?

Validation failures are caused by invoices that do not conform to the PINT AE XML standard, including missing mandatory fields, incorrect data formats, TRN mismatches, VAT calculation errors, or duplicate invoice references. The ASP checks every invoice against these rules automatically before transmission.

What happens if a company is not compliant after the mandate goes live?

Invoices issued outside the e-invoicing network will not have legal standing as tax records under UAE law. This affects VAT reclaim rights for buyers, creates gaps in the seller’s tax reporting, and may result in FTA penalties. Large trading partners and government-linked entities are also likely to reject non-compliant invoices operationally.

How can businesses avoid e-invoicing errors before going live?

Start with an ERP readiness assessment, audit your customer TRN data, confirm line-item VAT calculation logic, select an Accredited Service Provider early, and complete end-to-end testing with real invoice samples before your go-live date. These steps, done in order, eliminate the majority of compliance risks before they become live problems.

| Already have an ERP in place but not sure how it holds up against UAE e-invoicing requirements? Hitech can run a readiness assessment and identify exactly what needs to change before the deadline. |